Uwe E. Reinhardt is an economics professor at Princeton. He has some financial interests in the health care field.

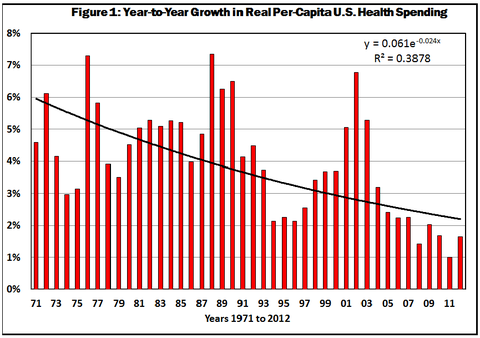

A hotly debated question among health policy wonks is whether the decline in the year-to-year growth in health spending in the United States, which started in 2002 (see Figure 1), will leave that growth rate at a permanently lower level.

I had a blog post on this question in January 2012, drawing no conclusion but noting that over the longer term the growth rate just had to come down closer to the level of growth in gross domestic product.

An intriguing question is what drives the fluctuations in the growth of

health spending clearly visible in Figure 1. It was a topic at a

recent symposium convened by the Altarum Center for Sustainable Health

Spending.

In a

joint effort, Thomas Getzen, professor emeritus of economics at Temple

University; Gary Claxton and Larry Levitt, senior vice presidents of the Henry

J. Kaiser Family Foundation, and Charles Roehrig, vice president of the Altarum

Institute, developed a statistical model in which the annual growth rate in

nominal national health spending (not adjusted for inflation) in any given year

over the long period 1965-2012 is assumed to be driven primarily by two

macroeconomic variables: (1) the inflation rate in the current and the previous

two years, measured by the G.D.P. deflator, and (2) the growth rate in real

G.D.P. in the current year, as well as in the previous five years. The approach

is called “lagged regression analysis.”

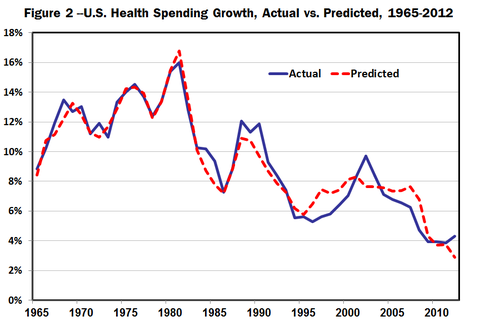

The model was able to explain 85 percent of the observed variation in the annual growth of national health spending, as is illustrated in the authors’ chart, which depicts the actual and the predicted growth rate in nominal health spending.

One concludes from this analysis that both year-to-year fluctuations in national health spending and the longer-term trend in that growth rate are driven primarily by current and prior-year changes in macroeconomic conditions.

One also infers from the model that if either inflation or the growth in real G.D.P. in the United States should pick up again, then the growth of national health spending should be expected to pick up again as well.

There is an emerging consensus among health economists, however, that other factors within United States health care itself have contributed to the decline in health spending growth and will prevent that growth rate from returning to levels observed in previous decades.

In a paper in the health policy journal Health Affairs, which devoted most of its May 2013 issue to health spending, the Harvard economists David Cutler and Nikhil Sahni explore health spending during the last decade only. They conclude that the recession of 2007-9 contributed only 37 percent of the decline in the growth rate in health spending during 2003-12, that another 8 percent can be explained by certain structural changes in the United States health system and that about 55 percent of the decline remains unexplained.

Among these other factors they list more cost-sharing by patients, less rapid development than was seen in the 1980s and 1990s of expensive new medical technology, including pharmaceutical products, and greater efficiency in the delivery of health care in response to downward pressure on revenue growth (in this connection, see also a paper by Kenneth Kaufman and Mark Grube).

In a similar vein, John Holahan and Stacey McMorrow of the Urban Institute conclude from their review of health spending trends in the last decade that macroeconomic conditions certainly were a primary factor in the lower health spending growth in recent years, but that other factors played a role as well, among them growing income inequality and the resulting decline of real income for millions of Americans, a decline in the number of Americans with employment-based health insurance and an accompanying increase in Medicaid enrollment as well as greater cost sharing by patients under private health insurance.

Now it will be noted in Figure 1 that a pronounced decline in the annual growth of health spending is not unique to the period 2002-12. There was a similar decline during 1989-96, only to end up in a sharp reversal. So is this time different?

In 1989-96, it was widely thought that “managed care” would be able to permanently subdue what was called the “health care cost monster.” Private health plans had gained leverage over the providers of health care through selective contracting, which meant that the plans would channel their insured only to a restricted network of doctors, hospitals, pharmacies and other providers of health care who were willing to make price concessions and tolerate external utilization control by the plans. Health plans could not, of course, actually dictate what physicians and patients could or could not do, but they could refuse to pay for particular procedures or added inpatient days in the hospital.

These various strictures imposed on doctors and their patients worked for about half a decade. By the mid-1990s, though, a nationwide backlash rose against managed care, swiftly seized upon under the banner of “Patients’ Bill of Rights,” by political entrepreneurs including President Clinton, who, ironically, had earlier based his own health reform plan on managed care. I describe it all in a paper, “The Predictable Managed Care Kvetch on the Rocky Road From Adolescence to Adulthood” (which, by the way, begins with a fake White House memorandum that apparently fooled more than few people).

To preserve industrial peace among employees chafing under the strictures of managed care, employers swiftly asked their agents in the health care market — the health plan – to relent, to substantially broaden their networks of providers and to ease up on utilization controls. By the end of the decade, it was business as usual in health care in the United States, as can clearly be seen in Figure 1.

Although I cannot be sure, I speculate that two developments since then have made a repeat performance of the later 1990s unlikely in the years ahead.

First, there have been enormous advances in health information technology, putting more and more of the traditionally opaque health care industry into statistical fishbowls that reveal to the world information on both the quality and the prices of health care. As I noted in my previous post, this greater transparency will make it possible to force real price competition on the supply side of the health system, including the powerful instrument of reference pricing.

Second, for the foreseeable future — in contrast to the late 1990s, when the American economy was booming and labor markets were tight — economic growth is likely to be relatively sluggish, as will be labor markets for all but highly skilled workers. It is my theory, forged by the experience of the 1990s, that under employment-based health insurance attempts at cost control will fail unless there is high unemployment.

Employees who worry about keeping their jobs or unemployed workers desperately seeking jobs are more likely to accept limits on their health insurance, along with higher levels of cost sharing, including reference pricing.

In the three decades preceding 2002, health spending in the United States tended over the longer run to grow two percentage points a year faster than did G.D.P. Absent periods in which G.D.P. declines sharply, I would be surprised if health spending in the future grew even one percentage point faster than G.D.P. The actual differential may well be south of that.

This post has been revised to reflect the following correction:

Correction: August 16, 2013